Table Of Content

- Advantages of having a larger down payment

- Bankrate logo

- Virginia Beach accountant pleads guilty to stealing from client, using pandemic funds on house down payment

- Sample loan programs

- Fannie Mae and Freddie Mac Programs (3% Down)

- Does your down payment affect your monthly mortgage payments?

- FAQ about down payments

- Different Types of Mortgage Loans for Buyers and Refinancers

With the median home price in 2023 at over $425,000, the average homebuyer would need $85,000 just for the down payment. DTI represents how much of your monthly income is used to pay off debt, and most mortgage lenders require a DTI around 43% or lower. A high DTI can hurt your chances of getting approved for loans or new credit. If you want to apply for other loans or buy a second home, borrowing less by putting more down can help keep your DTI ratio manageable. A 20% down payment would keep many home buyers locked out of the housing market. Fortunately, 20% is no longer the benchmark for a down payment on a house.

Advantages of having a larger down payment

Participating national banks and credit unions may also offer first-time home buyer grants. Depending on the program, you can use the funds for various purposes, such as covering your down payment, closing costs or necessary improvements and repairs. You can be eligible for more loan programs and competitive rates with a low debt-to-income (DTI) ratio. Lenders use your DTI to estimate how much you can afford for a monthly payment and may require a larger down payment to have a suitable ratio.

Bankrate logo

Her creative talents shine through her contributions to the popular video series "Home Lore" and "The Red Desk," which were nominated for the prestigious Shorty Awards. In her spare time, Miranda enjoys traveling, actively engages in the entrepreneurial community, and savors a perfectly brewed cup of coffee. And you may even be able to buy a home with no money down if you qualify for a VA or a USDA loan. You’ll need to put 20% down to avoid paying private mortgage insurance (PMI) on a conventional mortgage loan.

Virginia Beach accountant pleads guilty to stealing from client, using pandemic funds on house down payment

In comparison, FHA loans are available for 3.5% down with no first-time buyer or income restrictions. IRA—The principal contributed to a Roth IRA (individual retirement account) can be withdrawn without penalty or tax. In contrast, contributions from a traditional IRA will be subject to regular income tax as well as a 10% penalty if the contributions are withdrawn prior to the age of 59 ½. The funds can also legally be used to purchase a home for a spouse, parents, children, or grandchildren. The only caveat is that the home-buyer is only given 120 days to spend the withdrawn funds, or else they are liable for paying the penalty. Spouses can each individually withdraw $10,000 from their respective IRAs in order to pay $20,000 towards their down payment.

US Cities with Astronomical Down Payment Costs - AOL

US Cities with Astronomical Down Payment Costs.

Posted: Sat, 27 Apr 2024 23:00:00 GMT [source]

According to insurance provider MGIC, PMI would run around $120 per month for a borrower with a credit score of 760 who takes out a 30-year mortgage for a $400k house with 5% down. Also, in the U.S., the Department of Veterans Affairs (VA) has the ability to subsidize VA loans, which do not require a down payment. Only two other entities, the USDA and Navy Federal, allow the purchase of a home without a down payment. For more information about or to do calculations involving VA mortgages, please visit the VA Mortgage Calculator. If the amount of upfront cash available and down payment percentages are known, use the calculator below to calculate an estimate for an affordable home price. You’ll have to repay these loans if you move before the forgiveness period ends.

Fannie Mae and Freddie Mac Programs (3% Down)

Before considering how much money you need for a down payment and whether you’ll need assistance to cover it, start the process of getting preapproved for your mortgage. That way, you know how much house you can afford before saving for a down payment and closing on a property. Some programs offer a percentage based on the home’s sale price, while others cap assistance at a certain dollar amount. When looking at programs to apply for, research their requirements, whether it’s a grant or a loan, and how much assistance you can receive. Eligibility is determined by your household income and credit history, and it varies by state and program. The best mortgage lenders will work with you to see which assistance programs you’re eligible for.

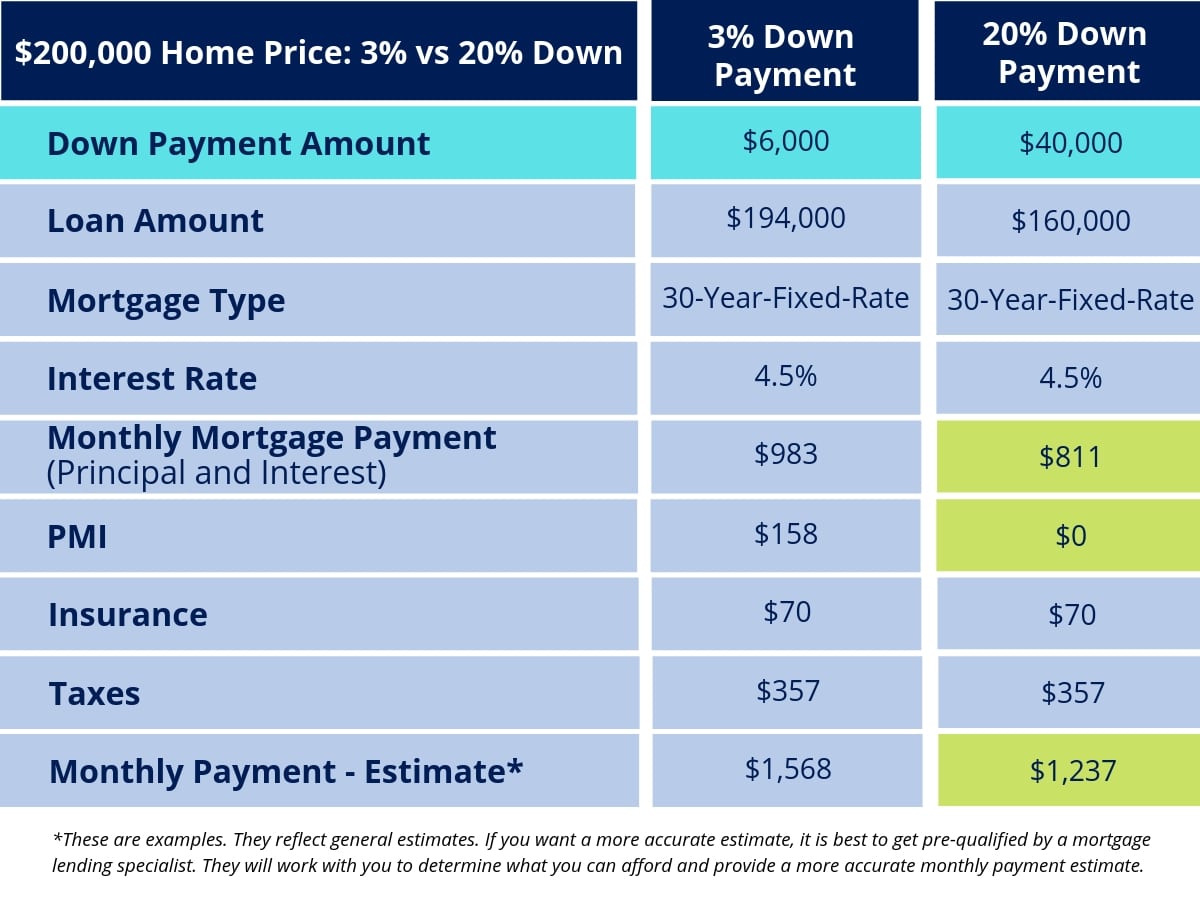

Does your down payment affect your monthly mortgage payments?

The higher your down payment, the more attractive you are to lenders. And just a 1 – 2 mortgage point drop in your interest rate can save you thousands of dollars over the life of your loan. A bigger down payment can make it easier to get approved for a mortgage and allow you to buy more house for the same monthly payment, or even less.

FAQ about down payments

Paying a larger down payment of 20% or more, if possible, usually lead to qualification for lower rates. Therefore a larger down payment will generally result in the lower amount paid on interest for borrowed money. For conventional loans, paying at least a 20% down payment when purchasing a home removes the need for Private Mortgage Insurance (PMI) payments, which are sizable monthly fees that add up over time. As already noted, down payment assistance comes in the form of grants, loans and other programs, and it’s typically reserved only for borrowers who qualify as first-time home buyers. Down payment assistance programs can be run by a variety of organizations, including the U.S.

Different Types of Mortgage Loans for Buyers and Refinancers

These programs, which usually offer assistance with down payment grants, can also help with closing costs. The U.S. Department of Housing and Urban Development lists first-time homebuyer programs by state. Select your state, then “Homeownership Assistance,” to find the program nearest you. There are a number of government programs available to prospective homebuyers who are struggling to come up with a down payment.

It’s possible to qualify for a conventional mortgage with a down payment as low as 3% of the final home purchase price. Private Mortgage Insurance (PMI) is calculated based on your credit score and amount of down payment. If your loan amount is greater than 80% of the home purchase price, lenders require insurance on their investment.

If you’re required to make a down payment, you might put down between 3 percent and 20 percent of the home’s purchase price, depending on your savings and what type of mortgage you’re getting. Redfin reports that the median home sales price in the United States is $411,887. The 20% down payment rule is now a thing of the past; the average first-time homebuyer puts down about 8% of the home’s purchase price.

“Expert verified” means that our Financial Review Board thoroughly evaluated the article for accuracy and clarity. The Review Board comprises a panel of financial experts whose objective is to ensure that our content is always objective and balanced.

However, this still represents $32,950 for a down payment on an average home—a hefty amount for most people. Add in closing costs, moving expenses and needed home maintenance and the total becomes even more daunting. That’s just the cutoff many lenders use for requiring private mortgage insurance (PMI) on a conventional loan. If you put less than 20% down, leave some wiggle room in your budget to account for the cost of monthly mortgage insurance payments. You generally need to put 20% down to avoid paying private mortgage insurance (PMI) on a conventional loan. PMI istypically a monthly fee that gets added to your monthly mortgage payment or is paid upfront by the lender in exchange for a slightly higher interest rate.

No comments:

Post a Comment